Conventional wisdom treats funding downturns as a threat to innovation — a period to survive, not to build. The history of disruptive companies tells a different story. Some of the most consequential businesses of the past two decades were founded not during periods of abundant capital and optimistic markets, but during exactly the kind of constrained, uncertain environment that exists right now.

The mechanism behind that pattern is worth understanding clearly — because it has direct implications for how founders and innovation leaders should be thinking about the current moment.

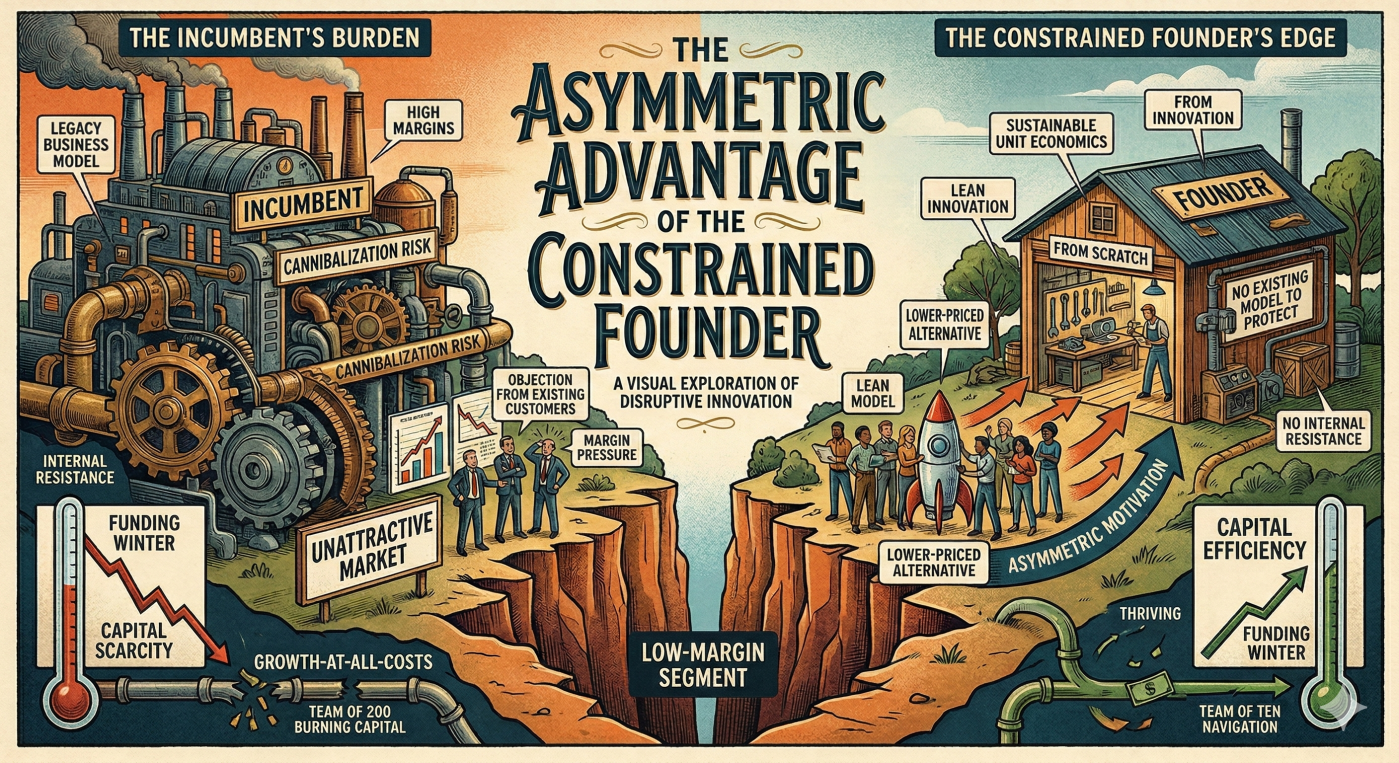

Christensen’s Framework, Applied to the Current Moment

Clayton Christensen’s disruptive innovation framework, introduced in The Innovator’s Dilemma, identifies a structural pattern that plays out with remarkable consistency across industries and market cycles. Incumbent companies, under pressure to defend margins and satisfy existing high-value customers, systematically move upmarket — improving their products and pricing for their most profitable segments while implicitly abandoning the lower end of the market.

This is rational behaviour for an incumbent. The economics of serving premium customers are better. The metrics that boards and investors track reward margin improvement over market expansion. The organisational structures of large companies are optimised for serving existing customers well, not for pursuing low-margin segments that don’t fit the current business model.

The structural consequence is predictable: segments that incumbents consider unattractive or unprofitable get underserved. And underserved segments are precisely where disruptive opportunities form.

Why Downturns Accelerate the Pattern

What a funding downturn adds to this dynamic is acceleration and amplification. When capital contracts and growth-at-all-costs strategies become unsustainable, incumbents don’t just drift upmarket — they retreat there deliberately and quickly. Cost structures get rationalised. Product lines get pruned. Expansion into adjacent or lower-margin segments gets deprioritised or abandoned. The strategic focus narrows to defending the core.

Every defensive move an incumbent makes in a downturn creates a corresponding opening. A customer segment that gets deprioritised becomes available. A product category that gets cut becomes contestable. A geographic market that gets abandoned becomes accessible. The incumbent’s rational response to constraint is the disruptor’s strategic opportunity.

The historical evidence for this pattern is compelling. Airbnb, Uber, and WhatsApp were all founded during or immediately after the 2008–2009 recession — a period of significant capital constraint and incumbent retrenchment. Slack emerged from a failed gaming company pivoting during a difficult market. These weren’t accidents of timing — they reflect the structural reality that constrained environments create strategic openings that abundant environments close off.

The Asymmetric Advantage of the Constrained Founder

The insight at the heart of Christensen’s framework is about asymmetric motivation — the recognition that what looks unattractive to an incumbent can look compelling to a disruptor, precisely because their competitive constraints are different.

An incumbent cannot profitably serve a low-margin segment without cannibalising its existing business model. A founder building from scratch has no existing business model to protect. The segment the incumbent finds unattractive is the segment the founder can build around without internal resistance, without margin pressure from a legacy product line, and without an existing customer base that would object to a lower-priced alternative.

This asymmetry is most pronounced in a downturn for a specific reason: the capital scarcity that makes growth-at-all-costs strategies unsustainable for incumbents is less constraining for lean founders who were never building on capital abundance in the first place. A team of ten with sustainable unit economics navigates a funding winter differently from a team of two hundred burning capital to maintain growth metrics.

What This Looks Like in Practice

The disruption opportunities worth paying attention to in the current environment are not the obvious ones — the large, well-served markets where incumbents are visibly strong. They’re the adjacent ones: markets that incumbents entered during the last period of capital abundance and are now quietly retreating from; customer segments that were never quite profitable enough to justify serious incumbent attention; product categories where the incumbent solution is expensive, complex, and over-engineered for what most customers actually need.

The pattern to look for is an incumbent optimising upward — adding features, raising prices, focusing on enterprise customers — while a large portion of the potential market sits underserved by a solution they can afford or easily adopt. That gap is where durable disruptive businesses form.

The discipline required is the same discipline discussed in the context of lean startup methodology: building the minimum viable version that serves the underserved segment well enough to generate genuine traction, rather than building the comprehensive solution that would satisfy the premium customer the incumbent is chasing.

The Timing Advantage That Compounds Over Time

The strategic value of building during a downturn isn’t just about capturing underserved segments in the short term. It’s about the compounding advantage that comes from being entrenched in those segments by the time capital returns and incumbents attempt to re-enter.

Incumbents that retreated from a segment during a downturn face a specific re-entry problem: the disruptor who moved in during their absence has customer relationships, product iteration cycles, and cost structures that are now optimised for that segment. The incumbent attempting to return has to compete against a company that has been focused on nothing else.

By the time market conditions improve and capital flows again, the strategic landscape has shifted. The incumbent that retreated finds itself facing a competitor in its own former market — one that is leaner, more focused, and structurally better suited to serve the segment that the incumbent abandoned.

The Strategic Frame Worth Carrying Forward

For innovation leaders evaluating where to place bets in the current environment, the Christensen lens offers a useful reorientation. The question isn’t “where is the market growing?” — in a constrained environment, that question leads toward the same crowded spaces where incumbents are also defending. The more productive question is “where are incumbents retreating — and what does that leave open?”

For founders navigating capital scarcity, the framing worth internalising is that the constraints that make this environment difficult for large incumbents are creating the exact conditions under which disruptive businesses historically form. Building lean, focusing on underserved segments, and developing sustainable unit economics are not just survival strategies — they are the foundations of the competitive position that becomes most valuable when conditions eventually improve.

Where are you seeing incumbents retreat in your industry — and what segments are becoming available as a result? The disruption curve is always in motion. The question is whether the current moment is being read clearly enough to act on it. Let’s keep learning — together.

Share your thoughts